The housing market is stressed. Mortgage rates have skyrocketed off historic lows and housing inventory has stalled. Millions of would-be homeowners are being forced to rent, fueling higher rental prices across the country. But challenges for one part of the housing market mean opportunity for another, and homebuilders are turning these lemons into lemonade with build-to-rent (BTR) communities. Smart property managers are also taking note.

There are of course two major, very different rental categories: single-family rentals and multifamily apartments. While property management companies — and the tech providers they rely on — service both these categories, the market is very segmented.

Housing segments include luxury, vacation or short-term rental (STR), condominiums, duplexes, high-rises, affordable housing and everything in between, with further segmentation across service offerings and tech stacks.

Build-to-Rent

The BTR segment includes horizontal apartments, duplexes, side-by-side row homes and small lot builds that are intended as rentals. Think of freestanding homes on clustered suburban lots between 600 and 5,000 square feet, or more spacious apartments that share a common wall.

Historically most signficant and noticeable in Texas and other Southwest states, build-to-rent housing has steadily grown in importance for single-family rental management firms, developers and investors across the U.S. through and following the pandemic.

According to National Association of Home Builders‘ analysis of the Census Bureau’s Quarterly Starts and Completions by Purpose and Design, there were approximately 21,000 single-family build-to-rent (SFBTR) starts during the second quarter of 2022, a 91% increase compared the second quarter of 2021. 69,000 BTR homes began construction over the last four quarters, a 60% increase over the 43,000 estimated SFBTR starts in the four quarters prior.

U.S. Census data also suggests that close to 5% of all single-family houses that developers have started to build in 2022 are planned as rentals, That’s up almost 2% percentage points from 10 years ago, with 6% of lots and land purchased by homebuilders in Q4 of 2021 bought by BTR companies.

While this ramp-up started before recent rate hikes and the ongoing chill in home sales, resulting demand for rentals has continued to pour gas on the rental market. Over 94.9% of single-family rental properties were occupied in the fourth quarter of 2022, with most major property management firms reporting 95%+ occupancy.

“That’s the highest occupancy rate in 25 years,” John Burns Real Estate Consulting CFO Don Walker told Wealth Management. “The occupancy rate has been inching higher for years, up from a low of around 95 percent in 2006.”

Construction’s bigger picture

At the same time, new construction could potentially help to equalize the overarching real estate market, which is suffering a nationwide deficit of 5 million single-family homes and slowdowns in development. I say “help” lightly, because build-to-rent is still a somewhat small piece of overall home construction — only 4% of the 1.8 million housing units estimated to start in 2022 are likely to be rented (between 50,000 to 72,000 units).

Brad Hunter, founder of Hunter Housing Economics, believes that number could be higher, estimating that 105,000 of the country’s new homes are build-to-rent developments and predicting a 50% growth in that figure by 2025. That difference could be attributed to homes sold by builders to third-parties party for rental purposes, which NAHB estimates may represent another 5% of single-family starts based on industry surveys.

The 13,000 single-family build-to-rent starts during the first quarter of 2022 also represented a 62.5% increase year-over-year, according to NAHB.

Homebuilders are also adding wood to the build-to-rent bonfire, with some of the nation’s largest developers, including Toll Brothers, D.R. Horton and Lennar, investing billions into single-family rentals, according to a recent Washington Post report.

“Home builders were not doing a good job of producing affordable homes for young families before this,” Hunter told the Washington Post. “Millennials are getting dogs, they’re having children, they’re working from home and they’re saying, ‘I need to move out of my downtown apartment and into a single-family home because I want a yard and parks nearby.’ But they can’t afford to buy.”

What does this mean for homebuyers?

Although build-to-rent construction could eventually impact housing supply, many developers and investors hold onto buildings for the long term or sell them to other rental investment firms.

Abha Bhattarai, the economics correspondent who wrote the recent Washington Post article, says that in addition to increasing rent figures, developers and investors alike are also focusing on build-to-rent due to appreciation of land values.

“So this is a new phenomenon that we’re seeing home builders get in on, as well as investors. There’s a lot of demand for this because, as you know, land values are appreciating, as are rents,” Bhattarai said, in an interview with Texas Standard. “And so I think a lot of folks are realizing that, ‘Hey, we don’t have to sell these houses just yet. We can rent them out. Rents are very high, and we can hold on to that very valuable land underneath the houses.'”

Housing economists have noted a shift toward rentals could disadvantage potential homebuyers, claiming that build-to-rent housing is actually replacing entry-level housing supply and creating more barriers to homeownership.

“We are replacing the supply of available starter homes with even more rental housing,” said James Gaines, an economist at Texas A&M University’s real estate research center, in another interview with the Washington Post. “It’s shifting the economic dynamics for entry-level home-buying and has a real impact on what kind of houses people can get and how much they can get them for.”

While build-to-rent may have negative consequences for the macro housing market and home buyers at large, that isn’t stopping renters from flocking to these properties.

As opposed to those who were able to lock in low, fixed-year mortgage rates during the pandemic, a growing wave of forced renters are now dealing with rising rent prices — without the benefit of an appreciating asset.

As pockets are emptied to pay mounting rents, it would seem that some people who were close to homeownership during the pandemic may now be even further away from buying their first home. Unfortunately for this demographic, foregoing shelter is not an option.

Instead they have to make a choice: attempt to squeeze a growing family into a multifamily apartment unit, or move into the growing supply of “spacious” build-to-rent single-family homes.

“On the whole, millennials in particular – you know, the folks who are in their late 20s, 30s and early 40s – came of age during the financial crisis. They have dealt with hurdle after hurdle, and many of them just don’t have the cash for a down payment. But at the same time, they’re getting dogs, they’re having children. They’re deciding they need homes of their own. So these have become a great solution for them,” Bhattarai told Texas Standard.

Apartment demand slows

This shift can perhaps be seen in apartment demand, with RealPage reporting that apartment demand fell by 82,095 units in the third quarter for a year-to-date net demand of -47,143 units. The report also notes that this is a typically strong leasing period, and states this is the first time that demand registered negative during the third quarter period since it began tracking apartments (30 years).

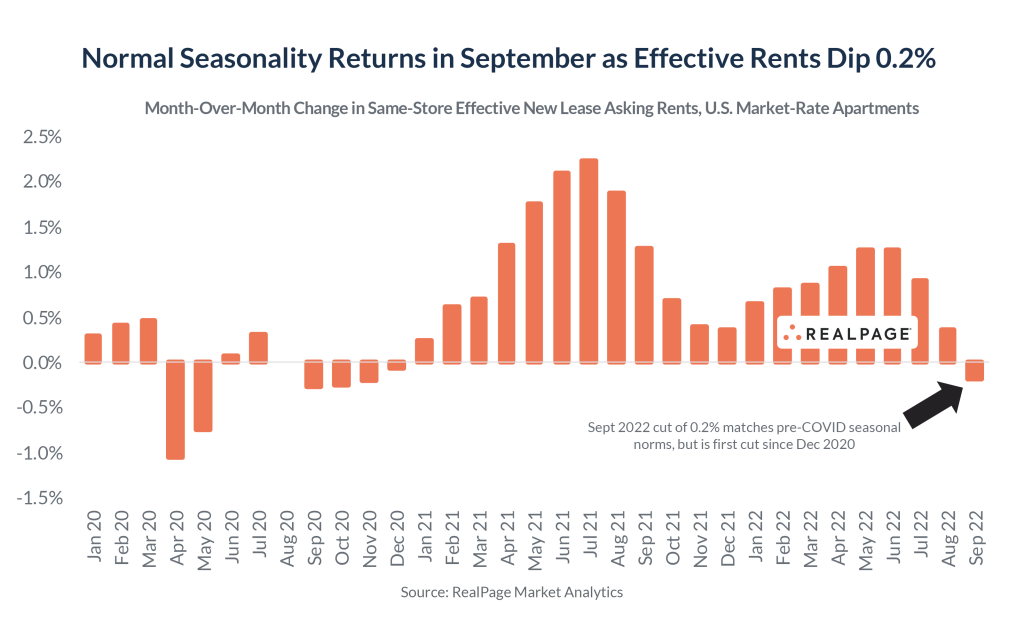

RealPage says this has contributed to slowing rent increases during 2022 as compared to 2021, with month-over-month demand (-0.2%) falling in September for the first time since December 2020, but also noted this coincides with mild historical dips each September.

While rising rent could be contributing to that weakened demand, the report noted that demand has softened for apartments at all price points in almost all markets of the country, and found that household incomes among new leasers jumped 13% year over year through August (keeping rent-to-income ratios above 23%).

RealPage says that the market would be seeing stronger demand pushing into Class C apartments and more affordable cities if affordability was the major driver of softening apartment demand, and instead says that these measures point to low consumer confidence.

Recent month-over-month changes in effective asking rents have also registered below 2021 in every month since April, falling from a 15.7% year-over-year rent growth peak in March to just 9% in September.

The report says this is the first single-digital YoY growth number since summer of 2021, and stated that peak rent growth is “clearly in the rearview mirror.”

“Apartment demand is cyclical while apartment supply is structural. We are structurally undersupplied, with vacancy rates stubbornly low even long before COVID. Many of these new projects will likely face prolonged lease-up periods but in the long run, they’ll fill up,” the report states, claiming that new apartment starts are also expected to drop from multi-decade highs due to higher financing costs and softening fundamentals.

It also showed that while demand weakened slightly in most markets, there were more sizable vacancy gains (1.5%) in desert markets (Phoenix, Las Vegas) and Florida (Tampa, Ft. Lauderdale, Orlando, Jacksonville, West Palm Beach), lending further credence to the movement out of apartments and into single-family rentals.