Qualia, the digital real estate closing platform, recently released its 2022 Homebuyer Sentiment Index, which surveyed more than 1,000 recent and prospective homebuyers. The results indicate that lenders must turn their attention to improving the closing experience they provide their borrowers in order to win repeat business and earn referrals. The following is an excerpt from the “Financing A Home” section of that report.

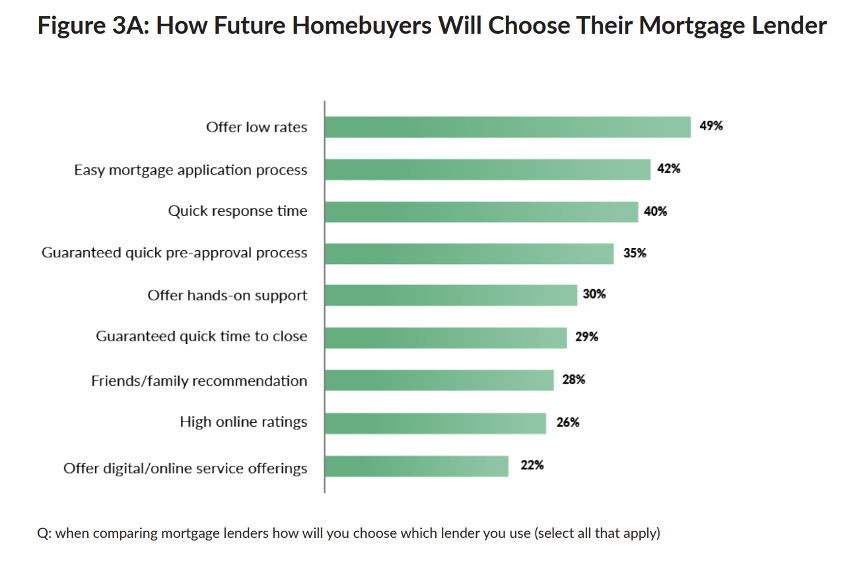

In Qualia’s summer 2021 survey of homebuyers, the vast majority of borrowers reported that they leveraged online tools to apply for their mortgage. To better understand how these point of sale (POS) systems impact borrower decisions to work with a lender, Qualia added a new question to the survey in 2022, asking future borrowers “when comparing mortgage lenders how will you choose which lender you use?” The highest-selected answer was “low rates” (49%) followed by “easy mortgage application process” (42%) and “quick response times” (40%). These responses underscore the value of POS systems for meeting borrower expectations for an easy and quick application process.

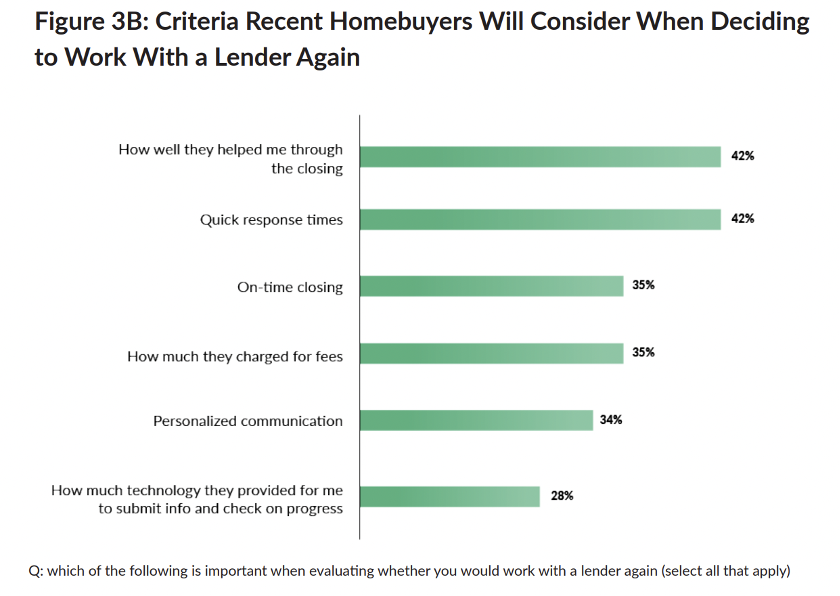

While POS systems are beneficial for acquiring borrowers, the closing process seems to be the most important factor for consumers when it comes to working with a lender again. When recent borrowers were asked “which of the following is important when evaluating whether you would work with a lender again?” The top 4 responses were “quick response times,” (42%) “how well they helped me through the closing,” (42%) and then followed by a tie for “on-time closing” (35%) and “how much they charged for fees” (35%).

These responses indicate that lenders must start shifting their attention toward improving the closing process. For the past several years, POS technology has become nearly ubiquitous among lenders. Now, lenders must turn their focus to backend technology that helps them streamline and automate their workflows—especially those with title & escrow companies. This backend, infrastructural software is the technology that consumers don’t typically touch or see; however, it greatly impacts their overall experience.

Backend technology that automates and connects aspects of the mortgage processing workflow can also improve the consumer experience by reducing the number of times borrowers need to provide the same piece of information. This technology works on the infrastructural level to not only connect internal workflows, but also to connect lenders with external parties such as title & escrow companies whose workflows often overlap with lenders during the pre-closing, closing, and post-closing processes. Oftentimes, transaction parties (real estate agents, lenders, title & escrow agents) each use their own siloed communication channel (sometimes referred to as a “point solution”) to interact with a homebuyer. This lack of connectivity creates a less-than-ideal borrower experience. For example, a borrower may provide a piece of information such as their address to a lender and then later be asked to provide that same piece of information to their title company. Our survey found that nearly one quarter (24%) were required to submit the same piece of information more than once during the mortgage process.

A primary solution to this challenge is creating connections with each party’s system of record. When lender systems are integrated with other parties’ systems, a borrower can provide a piece of information such as their address a single time, and it will populate across all relevant files on both the mortgage lender LOS and the title & escrow company’s title production workflow software. This creates a more efficient flow of information and eliminates the possibility of mismatched information within a lender and title company’s files.

According to a recent STRATMOR study, the failure to close a loan on the expected timeframe costs a lender 57 net promoter score (NPS) points. Those results further emphasize the business value of technology that simplifies communication with homebuyers and closing partners. Lenders who invest in connected platforms can provide quicker response times, meet partner expectations, and ultimately improve the homebuying experience.

Interested in reading the full report? Download Qualia’s 2022 Homebuyer Sentiment Index here.